*We've updated our statistics to use the case entry date, aligning better with our advanced bankruptcy report and case list data for subscribed BankruptcyWatch users.

Our Analysis of the Bankruptcy Statistics (Updated December 29th, 2025)

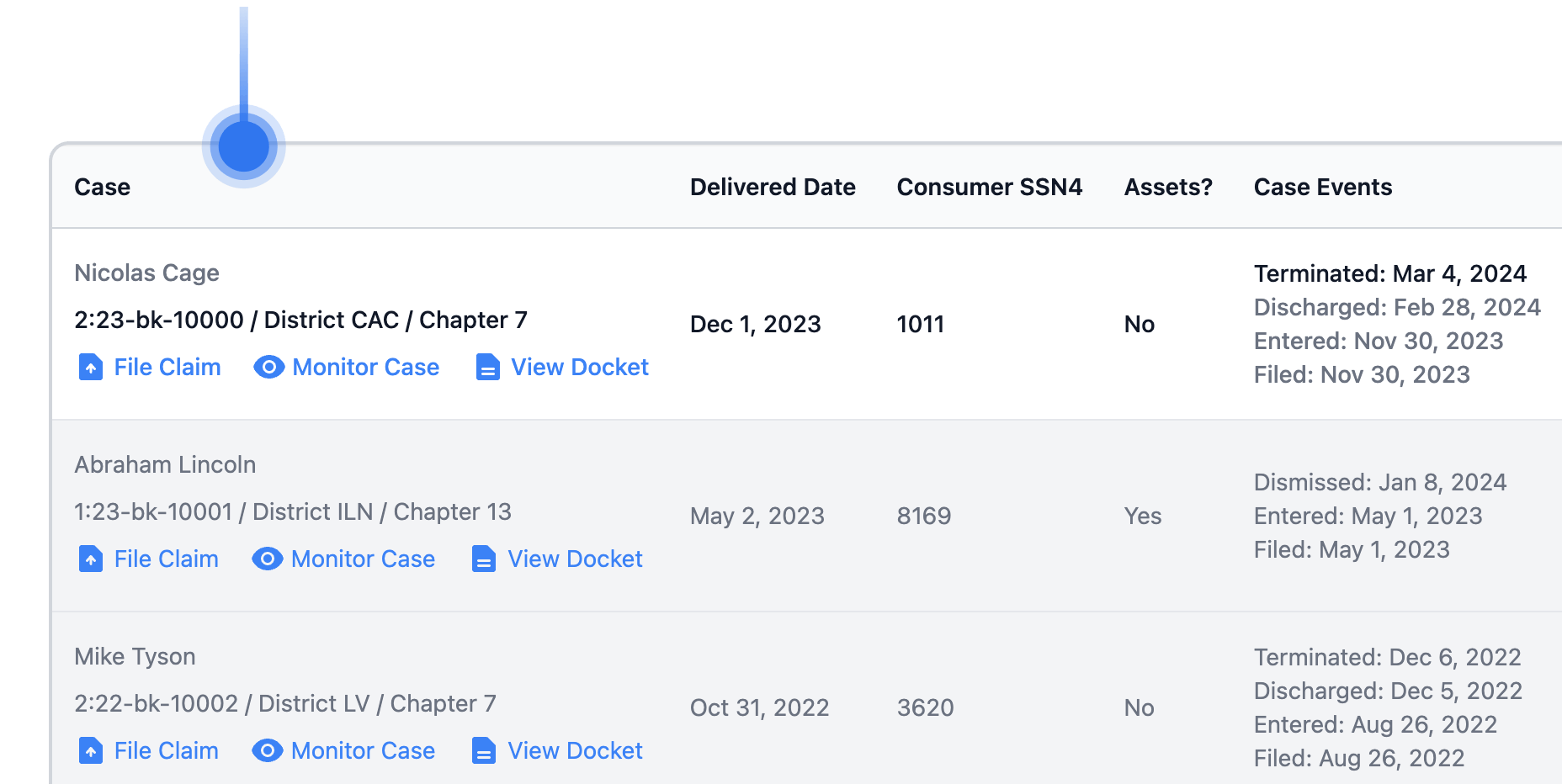

Week 52 closed out the year with significant year-over-year increases, with consumer bankruptcies rising approximately 22% compared with the same week last year. Chapter 7 filings, a lifeline for many struggling households, were up 14.13% year-over-year (6,235 in 2024 to 7,116 in 2025). Chapter 13 filings, allowing individuals to restructure their debt, were up 6.34% year-over-year (3,723 in 2024 to 3,959 in 2025). Chapter 11 filings, often used by businesses dealing with insolvency, were up 37.84% year-over-year (111 in 2024 to 153 in 2025).

As 2025 draws to a close, the bankruptcy landscape reveals a tale of two Americas. Homeowners insulated by pandemic-era refinancing and swelling property values remain largely protected—nearly half hold equity cushions worth double their mortgage balances. Meanwhile, consumers relying on unsecured credit face mounting pressure. This divergence explains why Chapter 7 liquidations are outpacing Chapter 13 reorganizations: those without home equity to tap are running out of options. The credit-driven nature of today's distress stands in stark contrast to the foreclosure crisis of 2008-2009, signaling that this cycle's pain points lie squarely in credit cards, auto loans, and personal debt.

The year-end data paints a sobering picture for 2026. With bankruptcy filings accelerating through the final weeks of 2025 and no relief in sight from elevated interest rates or living costs, lenders should prepare for sustained pressure on portfolio performance. The 22% surge in consumer filings and 38% jump in business bankruptcies suggest we're in the early-to-middle stages of this cycle, not the tail end. Strategic monitoring and proactive account management will be critical as we enter the new year.